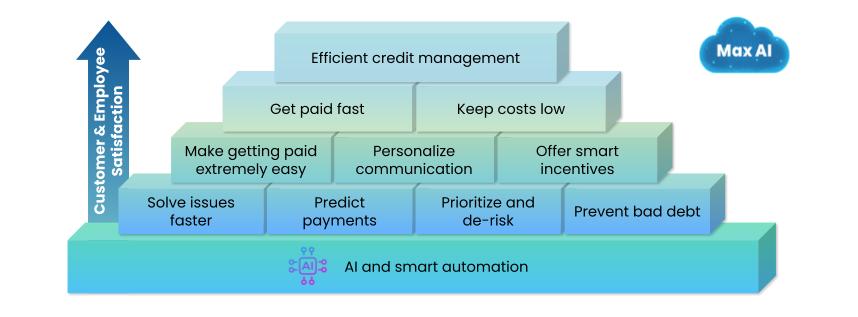

Use the 7 pillars of AI in Credit Management for more cashflow at lower cost

The AI-Powered Transformation of Credit Management: Seven Pillars for Unlocking Cash Flow and Driving Growth

Introduction: The New Imperative in Cash Flow Management

Getting paid has become increasingly uncertain. In the contemporary global economy, characterized by unprecedented volatility due to a cocktail of climate risk, war, geopolitical tension, and intense competition, the strategic management of cash flow has transitioned from a routine financial function to a critical determinant of corporate survival and growth. Businesses today operate within a complex ecosystem where manual processes, major logistical disruptions, escalating customer expectations for personalized service, and macroeconomic uncertainties create significant pressures on the order-to-cash (O2C) cycle.

Traditional credit management, often a reactive and labor-intensive discipline, is increasingly proving inadequate. It is a system burdened by static communication and inefficient workflows, leading to inflated Days Sales Outstanding (DSO), constrained working capital, and strained customer relationships. This traditional model operates on a flawed, brute-force paradigm—a high-cost, low-reward function that treats the O2C cycle as a zero-sum game.

Consider the waterbed analogy: to get results, the old method is to push down hard on one side with costly, adversarial tactics, such as threatening legal action against every late payer. While this intense pressure might force some payments up, it is incredibly expensive, creates immense friction, and damages the very customer relationships you aim to preserve.

The core purpose of the technological shift we are about to explore is to fundamentally redistribute the balance of this old model. The goal is to transform credit management into a highly efficient, relationship-building machine that positively affects stakeholders inside and outside of the organization. Instead of pushing down with brute force, AI allows us to apply precise, gentle “nudges” across multiple points simultaneously. This intelligent nudging—a personalized reminder here, a smart incentive there—elevates the entire system, resulting in faster payments and lower costs without sacrificing goodwill. This is achieved by increasing the quality of every touchpoint and by making financial processes transparent, seamless, and silky smooth.

Artificial Intelligence will be the engine for this transformation. This report delineates a comprehensive, interconnected framework for building this proactive and customer-centric O2C cycle, structured around seven pillars of AI-driven credit management. These pillars represent a holistic strategy for transforming how businesses manage receivables, mitigate risk, and engage with their customers, ultimately turning a traditional cost center into a strategic driver of growth and value.

Chapter 1: Dynamic Content with Generative AI

Chapter 1: Dynamic Content with Generative AI

Chapter 1: Dynamic Content with Generative AI

Chapter 1: Dynamic Content with Generative AIThe initial point of contact with a customer regarding an overdue invoice is arguably the most delicate and impactful stage of the entire collections process. It is here that the relationship can be either strengthened or irrevocably damaged. Historically, this has been the domain of generic form letters and impersonal call scripts—a one-size-fits-all approach that is demonstrably failing in the modern B2B landscape. The advent of Generative AI (GenAI) marks a definitive break from this legacy, introducing a new frontier where customer engagement is not just automated, but hyper-personalized, empathetic, and dynamically adaptive at an unprecedented scale.

The Paradigm Shift from Static to Hyper-Personalized Communication

The fundamental failure of traditional dunning lies in its impersonal nature. A generic reminder stating, “Your payment is overdue. Pay immediately to avoid additional fees!”, ignores the complex human and business realities behind a late payment. Such messages are not only easily ignored amidst the tsunamis of digital communication but can actively erode trust and induce anxiety, leading over 50% of customers to feel significantly stressed upon receiving a payment reminder. This stress often leads to avoidance, making the communication counterproductive. In one survey, 20% of respondents reported intentionally withholding a payment after receiving an upsetting call from a collector, highlighting the negative financial impact of poor engagement strategies.

Generative AI fundamentally inverts this model. Instead of broadcasting a single message to many, it crafts a unique message for each individual. By analyzing a customer’s entire history—including past payment behavior, inbound and outbound messages, issues and resolutions, communication preferences, and even the tone of previous interactions—GenAI can draft hyper-personalized repayment proposals, customized follow-up emails, and tailored call scripts. Executed well, and fed by unique and diverse data, this capability allows a system to generate communication that feels human, considerate, and context-aware, dramatically increasing the likelihood of a positive response. Done well, this strategy breaks free from the norm and the standard and highlights the power of credit management as a relationship building tool.

Consider two dunning emails sent for the same overdue invoice. The first is a standard template: blunt, impersonal, and demanding. The second is crafted by a GenAI engine by mining and aggregating data from CRM systems. It might read: “Hi Sarah, we’re writing about your recent invoice. We know you’re a valued partner and typically pay on time. We’re here to help you get back on track—click here to make a partial payment and start reducing your balance”. This message acknowledges the relationship, offers a flexible solution, and replaces anxiety with a clear, achievable next step. This shift from a transactional demand to a supportive interaction is the core of the GenAI paradigm in collections. You could get as personal as you prefer to allow yourself, adding payment behavioral statistics but also facts about recent legal changes in the company such as mergers and acquisitions discovered through external sources directly integrated with the credit management tool.

The Power of Dynamic, Two-Way Communication

Dynamic content generation is a two-way street. While GenAI excels at creating personalized outgoing messages, its value is magnified by its ability to intelligently process incoming customer communications. Using Natural Language Processing (NLP), the system can instantly read, understand, and categorize replies from emails, chat platforms, and customer portals. It can detect the customer’s intent (e.g., “I want to make a payment,” “I have a dispute,” “I need an extension”), identify key information, and automatically trigger the appropriate workflow. This instant distillation and orchestration of information means that a customer’s query can be routed for automated resolution or escalated to the correct human agent without delay, feeding directly into the end-to-end automation discussed in Chapter 4.

This capability is crucial for scaling personalized engagement. In a manual environment, a large workforce with diverse backgrounds and training levels will inevitably produce inconsistent communication. AI can ensure that every interaction, whether inbound or outbound, adheres to the company’s desired tone and strategy, creating a coherent and consistently positive customer experience.

The Empathetic Bot: Real-Time Adaptation and Sentiment Analysis

The true power of modern AI in customer engagement extends beyond simply drafting text; it lies in the ability to understand and react in real time. Leveraging advanced NLP, these systems can analyze customer replies, chat messages, and even the sentiment and tone of voice in phone calls. This allows the system to function as an “empathetic bot,” capable of gauging a customer’s emotional state and adapting its strategy accordingly.

We talk of agentic AI when the bot is completely embedded in the automatic processes of the organization. For instance, if a customer’s written response or vocal tone indicates stress or frustration, the AI can de-escalate the situation by shifting from a reminder to an offer of assistance, such as a flexible payment plan. This real-time sentiment analysis provides agents with immediate insight, flagging when a conversation is deteriorating and triggering automated playbooks with appropriate responses to protect the customer relationship. One case study demonstrated that a GenAI-powered voice assistant, by adjusting its tone based on customer sentiment, successfully reduced the need for human agent escalations by 17%.

This capability transforms a potentially adversarial interaction into a collaborative problem-solving session. A friendly, personal, and positive communication style elicits a friendly reaction, improving outcomes and reducing stress for both the customer and the collection agent.

This approach yields immediate and substantial results. Over 50% of companies report an immediate improvement in recovery rates after adopting GenAI, a gain largely attributed to this empathetic, automated approach that reduces friction and increases a customer’s willingness to pay.

Segmentation and Omnichannel Outreach: Precision at Scale

Hyper-personalization is made efficient through intelligent segmentation. We can use machine learning technology to analyze vast datasets to identify coherent customer segments based on behavioral patterns, risk profiles, and demographic data. This allows the organization to tailor distinct communication strategies for different groups—for example, a gentle, service-oriented approach for loyal, low-risk customers versus a more direct strategy for chronically late accounts. This segmentation allows the entire collections organization to align its resources and tactics effectively leaving room for very high quality touchpoints.

Furthermore, AI orchestrates these personalized messages across multiple channels. An omnichannel strategy that integrates email, SMS, and voice calls is demonstrably more effective than a single-channel approach. Data shows that omnichannel strategies can increase successful debt resolutions by 31% and achieve 2-3 times higher response rates than voice-only methods. AI determines the optimal channel and timing for each customer, ensuring the message has the highest probability of being seen and acted upon.

Quantifying the Impact on Recovery and Efficiency

The adoption of generative AI in customer engagement is not merely a qualitative improvement; it delivers powerful, measurable financial and operational gains. The data consistently shows that personalization and empathy are not soft benefits but hard drivers of performance. A McKinsey study found that personalization, if done well, in outreach can improve efficacy rates by up to 20%. Other analyses by Bloomberg and IBM corroborate this, citing at least a 10% improvement in effectiveness of AI-based personalization strategies which is coupled with a significant 40% reduction in operational expenses, as AI automates repetitive communication tasks and allows human agents to focus on more complex, high-value cases.

The impact on customer engagement metrics is equally dramatic. In one implementation, the use of GenAI to create tailored marketing and outreach led to a 4x increase in email campaign click-through rates, demonstrating that customers are far more likely to interact with content that feels relevant and personalized. This heightened engagement translates directly into faster collections and better payment outcomes. Marketing typically aims to sell to new customers they know little about, imagine applying this same logic to customers you know a lot about and have a deep personal history with. The following table consolidates key performance indicators, illustrating the multi-faceted value proposition of this pillar.

Table 1: Quantifiable Impact of Generative AI in Customer Engagement & Dunning

| Metric | Achievable Improvement | Key Insight | Source |

| Recovery Rates | 10-20% Increase | Personalization and empathy directly translate to higher payment success. | The promise of generative AI for credit customer assistance |

| On-Call Payments | 23% Growth | Real-time agent assistance and tailored plans convert conversations to payments. | Holistic customer assistance through digital-first collections | McKinsey |

| Promise-to-Pay (PTP) Rates | 18% Increase | AI-driven strategies lead to more reliable commitments from customers. | MaxCredible issue and reporting |

| Email Engagement | 4x Increase in Click-Through Rates | Hyper-personalized content is dramatically more effective than generic blasts. | Say Goodbye to Blast Emails – How AI Helps Your Personalized Email Marketing |

| Operational Costs | Up to 40% Reduction | Automation of repetitive tasks frees up human agents for high-value work. | Holistic customer assistance through digital-first collections | McKinsey |

| Agent Escalations | 17% Reduction | Empathetic AI voice assistants can resolve issues without human intervention. | 91% Resolution rate for 18.7% of the conversations. |

| Time to Collect | 6-74% Reduction | Increased efficiency and faster responses accelerate the entire collection cycle. | MaxCredible DSO impact studies |

While the data overwhelmingly supports the effectiveness of GenAI, a crucial nuance emerges from recent research. A study co-authored at Yale found that human borrowers are more willing to break promises to repay when those promises are made to an AI agent. The study revealed that initial contact from an AI caller could create a “repayment deficit” that human agents, even after taking over the account, could not fully reverse. This does not contradict the value of AI but rather defines its optimal role. The most effective strategy is not full automation but a sophisticated human-AI hybrid model. GenAI should be deployed to handle the vast majority of interactions at scale: initial reminders, simple queries, and personalized outreach. However, the system must be intelligent enough to recognize critical junctures—such as a customer expressing high levels of frustration or making a firm promise-to-pay—and seamlessly escalate the interaction to a human agent. This approach leverages the efficiency and personalization of AI while reserving the unique accountability-enforcing presence of a human for the moments that matter most, creating a system superior to what either could achieve alone.

Strategic Value: Transforming Collections into a Customer Retention Engine

Ultimately, the most profound impact of generative AI in credit management is its ability to elevate the collections function from a purely transactional, and often negative, touchpoint into a strategic tool for customer retention. A positive, empathetic, and helpful interaction during a period of financial stress can build immense brand loyalty and trust. When a customer feels understood and supported rather than harassed, the relationship is strengthened. By transforming the collections process into a constructive dialogue, businesses can not only recover outstanding invoices more effectively but also enhance customer lifetime value. In this new paradigm, GenAI is not just a tool for collecting debt; it is a strategic asset for building more resilient and profitable customer relationships.

Chapter 2: AI-Powered Predictive Cash Flow Forecasting

The ability to accurately forecast cash flow is the bedrock of sound financial management. It informs critical decisions regarding investment, capital allocation, and operational spending. Yet for many organizations, forecasting remains a reactive, labor-intensive exercise fraught with uncertainty. The traditional approach, heavily reliant on static historical data and manual spreadsheet manipulation, is ill-equipped for the dynamism of modern markets. AI-powered predictive analytics represents a fundamental leap forward, transforming forecasting from a periodic, backward-looking report into a continuous, forward-looking strategic function.

The Limitations of Traditional, Static Forecasting

Conventional cash flow forecasting is an inherently flawed process. Typically performed on a monthly or quarterly basis, it involves finance teams manually consolidating data from various systems, building models in spreadsheets, and chasing down inputs from different departments. This method is not only time-consuming and prone to human error but also suffers from a critical conceptual limitation: it primarily relies on lagging indicators. By extrapolating from past performance, it struggles to account for the complex interplay of variables that will shape future outcomes, especially in a volatile economic environment. The consequence of this approach is inaccurate forecasts that lead to frequent cash flow surprises. Businesses are left scrambling to plug unexpected financial gaps, often resorting to costly short-term borrowing or delaying strategic investments. Instead of proactively managing liquidity, finance leaders are forced into a reactive posture, constantly responding to crises rather than anticipating them. This static, periodic approach simply cannot move at the speed of modern business.

The AI Advantage: Precision Through Dynamic, Diverse Data

AI transforms forecasting by fundamentally changing the quality, quantity, and velocity of the data used for analysis. Instead of relying solely on historical internal data, AI-powered forecasting engines continuously ingest and analyze a vast and diverse array of data streams in real time. This includes structured data like payments, invoice volume, and customer demographics from ERP and CRM systems, live bank feeds, and transactional flows, as well as unstructured and external data like customer payment patterns, communication response times, industry trends, and even macroeconomic indicators.

By processing this massive volume of information, machine learning models can identify subtle, non-linear patterns and correlations that are completely invisible to manual human analysis. For instance, an AI might detect that a particular customer segment’s payment timeliness is highly correlated with a specific commodity price, allowing it to adjust inflow predictions with a level of granularity previously unimaginable. This ability to synthesize diverse, real-time inputs results in a dramatic and quantifiable leap in forecasting precision. Companies that have adopted AI-enabled forecasting report a 20% to 50% reduction in forecasting errors. In one documented case, an AI tool achieved an impressive 94% accuracy in its payment predictions, demonstrating the power of this data-driven approach.

Beyond Prediction: Intelligent Variance and Anomaly Detection

A key differentiator of AI-powered forecasting is that it moves beyond simply providing a number to providing an explanation. In traditional finance functions, when a forecast is missed, a time-consuming manual investigation must be launched to understand the cause. This involves hours of sifting through spreadsheets and reports to reconcile actuals against predictions.

AI automates this entire process. An intelligent forecasting system can instantly compare forecasted figures to actual results, detect anomalies, and automatically surface the key drivers behind any variance. For example, the system could immediately flag that a cash shortfall was caused by a combination of three large enterprise deals being delayed by one week and a slight slowdown in payment velocity from a specific geographic region. Crucially, it can also identify high-value invoices that were predicted to be paid but have not yet arrived, allowing the collections team to give these specific accounts special attention. This transforms variance analysis from a backward-looking audit into an actionable, strategic learning opportunity. Finance teams can move from asking “What happened?” to understanding “Why did it happen?” and, most importantly, “How can we improve next time?”.

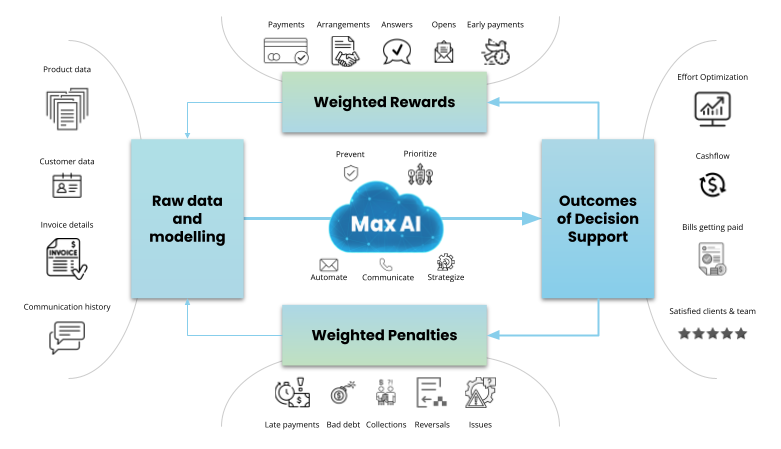

The Self-Improving Forecast: Reinforcement Learning

As all our users are unique with sometimes seasonal clients, these AI forecasting models are not static. The most advanced systems employ a technique known as reinforcement learning, where the model continuously learns and adapts based on its performance. The system treats the forecasting process as a series of decisions and receives “rewards” for accuracy and “penalties” for errors. It constantly analyzes the variance between its predicted payments and the actual incoming cash flow. When it detects a growing variance, it automatically adjusts its internal parameters to correct the error, effectively learning from its mistakes in real time.

This continuous feedback loop allows the model to become progressively more accurate over time, constantly refining its understanding of complex payment behaviors to maintain a high level of precision, often approximating over 90%.

Strategic Value: Optimizing Working Capital and Free Cash Flow

The strategic value of highly accurate cash flow forecasting is profound, extending directly to the balance sheet and the bottom line. The ultimate goal is to maximize Free Cash Flow (FCF)—the cash a company has left over after paying for its operating expenses and capital expenditures. FCF is a critical indicator of a company’s financial health and its ability to pay down debt, return value to shareholders, and invest in growth opportunities.

When a company cannot reliably predict its future cash position, it must adopt one of two defensive and costly strategies: either it maintains large, unproductive cash buffers to guard against unforeseen shortfalls, or it relies on expensive, short-term credit facilities to cover gaps as they appear. Both approaches are inefficient and erode profitability.

By using AI to anticipate cash flow with a high degree of accuracy weeks or even months in advance, a company can break this cycle. It gains the visibility needed to manage its working capital with much greater precision, reducing idle cash and freeing up capital for more productive uses. More strategically, it can plan its financing needs proactively, avoiding the premium rates associated with last-minute borrowing. Case studies by MaxCredible demonstrate that companies are able to achieve a 20% or greater reduction in its interest expenses directly as a result of the improved cash flow visibility provided by AI-driven forecasting. This illustrates that AI forecasting is not merely an operational accounting tool; it is a core strategic treasury function that directly lowers the cost of capital, strengthens financial stability, and improves overall profitability. Moreover a good forecast can contribute to optimal prioritization leveraging energy at the right time and place. More on prioritization in Chapter 4 and Chapter 5.

Chapter 3: Automated Payments and Smart Processing

Chapter 3: Automated Payments and Smart Processing

Chapter 3: Automated Payments and Smart Processing

Chapter 3: Automated Payments and Smart ProcessingThe moment a customer attempts to make a payment is a critical juncture in the revenue cycle. A seamless transaction strengthens the relationship and accelerates cash flow, while a failed payment introduces friction, frustrates the customer, and can lead to the silent but significant loss of revenue known as involuntary churn. Automating the payment process and applying intelligent logic to handle failures is a pillar of modern credit management that delivers outsized returns by preserving revenue streams and maximizing customer lifetime value.

The High Cost of Failed Payments and Involuntary Churn

A common misconception is that customer churn is primarily driven by dissatisfaction with a product or service. However, data reveals a different story. In many business models, particularly subscription-based services, up to 20-40% of customer churn stems from failed payment transactions, a phenomenon known as involuntary churn. These failures can be caused by a variety of mundane issues: an expired credit card, insufficient funds, or a temporary network glitch.

The financial impact of this friction is staggering. Failed payments can cost subscription businesses between 10% and 20% of their potential revenue through lost LTV, representing a massive and often overlooked source of leakage. The customer experience impact is equally severe. Research shows that 60% of organizations reported losing a substantial percentage of users who were lost due to payment errors. This highlights the critical importance of resolving these issues immediately and seamlessly. Each failed payment is not just a delayed transaction; it is a potential breaking point in the customer relationship.

The Power of the Smart Retry: From Static Rules to Intelligent Logic

The traditional approach to handling failed payments is rudimentary. Most systems employ a static, rules-based retry logic, attempting to process the transaction again at fixed intervals—for example, every 24 or 48 hours—regardless of the reason for the initial failure. This one-size-fits-all method is inefficient and can be counterproductive, as it may repeatedly attempt a transaction that has no chance of success (e.g., for a permanently closed account) while missing the optimal window for a temporary issue (e.g., insufficient funds that may be resolved a day later).

AI-powered “smart retries” represent a vastly more sophisticated approach. Instead of following a rigid schedule, an AI system analyzes the specific decline code provided by the payment processor to understand the root cause of the failure. It then tailors the retry strategy accordingly. For a “soft decline” like insufficient funds, the AI might leverage historical data to predict the day of the month the customer is most likely to have a positive balance and time the retry for that moment. For a “hard decline” like an expired card, it might halt retries and trigger a personalized communication asking the customer to update their details. This intelligent logic extends to optimizing the timing, frequency, and even the payment gateway used for each subsequent attempt, maximizing the probability of success.

The performance gap between these two methodologies is stark and well-documented. While traditional, static methods achieve a median payment recovery rate of approximately 30%, AI-powered platforms consistently deliver recovery rates in the range of 60-70% (source 1|source 2). This represents a 2x to 2.5x improvement over the standard logic embedded in most native billing systems. Even though the actual data is private and does not get published, multiple specific platforms have documented numbers approximating a 51% to 67% improvement in the conversion rate of the very first retry attempt, demonstrating the immediate impact of applying intelligent logic.

Table 2: AI-Powered vs. Traditional Payment Recovery

| Feature | Traditional (Static Rules) | AI-Powered (Smart Retries) |

| Core Logic | Fixed schedules (e.g., retry every 3 days). One-size-fits-all. | Dynamic, adaptive logic based on failure reason, customer history, and timing. |

| Average Recovery Rate | ~30% (Industry Median) | 60-70% |

| Key Differentiator | Simple to implement but inefficient. | Learns and improves over time; multi-dimensional optimization. |

| Impact on Customer | Can cause frustration with unnecessary notifications. | Minimizes friction and reduces involuntary churn. |

Diversifying Payment Options for Cost and Convenience

An intelligent payment processing strategy goes beyond simply managing failures; it proactively optimizes for success. AI can play a crucial role in diversifying payment options to enhance both customer convenience and cost-effectiveness for the business. By analyzing customer data—including industry, company size, and past payment behavior—an AI system can proactively offer the most suitable payment methods during the checkout or invoicing process.

For example, it might learn that smaller businesses prefer credit card payments for their simplicity, while larger enterprises favor ACH transfers for their lower transaction costs. By presenting the right options to the right customer at the right time, the system reduces friction in the payment process, increases the likelihood of a successful first-time transaction, and can strategically steer customers towards lower-cost payment rails, reducing the overall cost of payment acceptance for the business. This holistic approach ensures the entire payment experience is as seamless and efficient as possible. Reminding someone that they have a payment outstanding without immediately capturing that payment only makes it more difficult for the client to pay.

Strategic Value: Maximizing Customer Lifetime Value

The immediate, first-order benefit of a successful smart retry is the recovery of a single overdue payment. This, in itself, provides a clear return on investment. However, the true strategic value of this pillar is revealed when considering the second- and third-order effects. The second-order benefit is the prevention of involuntary churn, preserving the revenue stream from that customer for the following month.

The most profound impact, however, is on long-term customer retention. Data from Stripe, a leading payment processor and strategic partner of MaxCredible, reveals a critical finding: subscriptions that are recovered using smart retry tools continue, on average, for seven more months. This single statistic fundamentally reframes the purpose and value of this technology. It is not merely a transactional tool for payment processing; it is a powerful engine for customer retention. Every successfully recovered payment does not just save one invoice; it saves a significant portion of that customer’s total lifetime value (LTV). This multiplies the ROI of smart retry technology, transforming it from an operational efficiency tool into a core component of a company’s customer retention and growth strategy. By seamlessly resolving an issue that could have ended the relationship, the business preserves a long-term revenue stream and reinforces customer loyalty.

Preparing for the Next Wave: Stablecoin Payments

Looking ahead, the diversification of payment rails is poised to accelerate with the integration of digital currencies. Stablecoins, in particular, are emerging as a significant force in the future of transactions and will be part of our future, whether we like it or not. These digital assets, pegged to stable fiat currencies like the U.S. Dollar or the Euro, combine the technological benefits of cryptocurrencies with the stability of traditional money. The result is the potential for instant payments at a fraction of the cost of card networks and with significantly reduced financial and currency risk.

This evolution is not a distant prospect; an increasing number of providers are building the infrastructure to facilitate these transactions. Businesses need to be ready for it, as the ability to accept this new form of payment will become a competitive advantage, offering lower processing fees and meeting the demands of a digitally-native customer base. Forward-looking platforms must be prepared for this shift. To this end, MaxCredible offers payment integrations that are designed to be future-proof, ensuring clients are equipped to seamlessly incorporate stablecoin payments as they become a mainstream option.

Facilitating any form and shape of digital payments helps improve forecasting (Chapter 3), end-to-end automation (Chapter 4), and effectively speeds up your working capital generation (Chapter 5)

Chapter 4: End-to-End Automation of the Order-to-Cash Cycle

The order-to-cash (O2C) cycle is the lifeblood of any business, representing the complete sequence of operations from a customer’s order to the receipt and application of cash. In many organizations, this cycle is a fragmented and labor-intensive process, stitched together by manual handoffs and repetitive tasks. Each manual touchpoint is a source of potential friction, introducing delays, errors, and significant operational costs that lead to a higher DSO and a finance team perpetually bogged down in low-value work. The “touchless” revolution, powered by AI and end-to-end automation, aims to eliminate this friction, creating a seamless, intelligent, and highly efficient revenue cycle that transforms the role of the modern finance department.

Founding principle: E-Invoicing as the New Standard

The first point of failure in the traditional O2C cycle has always been the invoice itself—getting the right data to the right person in the right format. The advent of e-invoicing has rendered manual data capture technologies like OCR largely obsolete for best-in-class operations. E-invoicing ensures that invoice data is created in a structured, machine-readable format from the very beginning. Through compliant, interconnected networks, facilitated by MaxCredible partners like Unified Post, e-invoices are transmitted directly from the supplier’s system to the buyer’s accounts payable (AP) system.

This single technological shift eradicates an entire category of common payment obstacles. Issues such as the invoice being sent to the wrong email, landing in spam, being blocked by a firewall, or missing a mandatory Purchase Order (PO) number are effectively eliminated. The invoice arrives correctly, is instantly parsed, and is ready for processing, breaking the chain of missed or lost invoices and establishing a reliable foundation for the rest of the O2C cycle.

The “Formula 1 Pit Stop”: AI-Powered Obstacle Management

With guaranteed delivery solved by e-invoicing, the focus of automation shifts to what happens next. A manual process is reactive; an issue is raised by the customer, and only then does a team scramble to figure out what to do. An AI-driven approach is akin to a Formula 1 pit stop: a highly prepared, lightning-fast operation designed for immediate analysis and resolution of any payment obstacle.

When a customer raises a dispute—for example, via an email analyzed by NLP systems (as discussed in Chapter 1)—the AI can instantly:

- Detect and Categorize: Identify the nature of the dispute (e.g., pricing error, quantity discrepancy, missing proof of delivery).

- Gather Intelligence: Automatically pull all relevant information, data, and documents from various systems—the original purchase order, the invoice, shipping documents, and contract terms.

- Route and Recommend: Route the entire case file to the appropriate department or individual and, in many cases, suggest a resolution based on historical data and company policy.

- Solve using AI or an SOP: If the solution requires information, data, or a behavior that can be solved by a system, a fully automated solution can be produced (a new invoice can be sent, a discount applied, etc. If it requires a degree of manual intervention, the teams follow an efficient and effective SOP based on the previous effective resolutions of the issue.

This transforms dispute resolution from a multi-day manual investigation into a near-real-time process, drastically reducing resolution times and improving customer satisfaction.

Beyond Invoicing: Automating the Full, Prioritized Revenue Cycle

While intelligent dispute management is a powerful component, true end-to-end automation addresses the entire O2C lifecycle with an added layer of intelligence. AI’s role begins even before an order is placed, with automated credit risk assessments that can be performed instantly, ensuring that credit limits are appropriate and risk is managed from the outset.

Crucially, AI also prioritizes activities based on value and effort. By analyzing factors like invoice amount, customer risk profile, and the predicted cost to collect, the system can intelligently determine which actions are worth pursuing automatically versus which require human intervention. The smartest systems take things a step further and also take the current capacity of the Credit Management team into consideration. After intervention, or when an invoice is paid, AI streamlines cash application by intelligently matching payments to invoices with high accuracy, even with incomplete remittance details. It is increasingly common for digital payments to be matched up to 99.9% of the time. Thanks to the immediacy in invoicing and in payment reconciliation data is now available in real time throughout the entire workflow of a credit manager. AI is there to provide continuous, real-time monitoring, flagging exceptions and anomalies as they happen, not weeks later during a month-end close.

The oil to keep our formula one engine running is data. To enable and facilitate a self-learning credit management system input and output data needs to be generated every step of the way. Where traditional systems should no longer be falling short because of inaccurate payment information, the next generation of systems will rely on even more inclusive end-to-end data creation. Considering that e-invoicing already governs invoice delivery, partnering with an email delivery and receipt platforms like “aangetekend mailen” could further complete the invoice communication data chain, whilst facilitating a significant reduction in carbon costs versus traditional methods (registered letters). In sum, all the parts and elements of the Credit Management workflows and value chains need to be consistently evaluated for additional data creation possibilities.

Strategic Value: Elevating the Finance Function

The primary benefits of O2C automation—efficiency gains and cost savings—are compelling on their own. The secondary benefit is a significant improvement in accuracy, which reduces errors, extra work, and financial risk. However, the most profound and strategic transformation lies in what happens to the human team when they are liberated from the drudgery of manual, repetitive tasks.

When credit managers and finance professionals are no longer consumed by manual processing, their roles and capabilities are fundamentally elevated. They are redeployed from transactional work to high-value strategic initiatives. Their valuable time, experience, and insights can now be dedicated to analyzing the rich data generated by the automated system, optimizing credit management strategies, enhancing cash flow forecasting, and managing key customer relationships.

This shift transforms the credit and even finance department’s identity within the organization. It ceases to be a reactive, back-office cost center and evolves into a proactive, data-driven strategic hub. Armed with real-time visibility and freed from manual constraints, the finance team becomes an engine for value creation, providing the critical insights that guide better, faster decision-making across the entire business. This elevation of the finance function is the ultimate strategic outcome of the touchless revolution.

Chapter 5: Working Capital Optimization and Smart incentives

In the intricate dance of B2B commerce, the timing of payments is a critical factor that directly impacts the financial health of both buyers and sellers. Working capital, calculated as current assets minus current liabilities, is the lifeblood of a company, measuring its ability to fund daily operations and meet short-term obligations. For sellers, accelerating cash inflows is key to maintaining liquidity. For buyers, optimizing cash outflows is essential for managing working capital. The traditional, rigid approach to payment terms often creates a zero-sum game. The emergence of AI-powered smart incentives, particularly dynamic discounting, transforms this dynamic into a collaborative, win-win strategy that optimizes working capital across the supply chain.

The Evolution from Static Discounts to Dynamic Incentives

The most common form of early payment incentive is the static discount, famously encapsulated by terms like “2/10, net 30.” This offers a fixed 2% discount if an invoice is paid within 10 days, with the full amount due in 30 days. While straightforward, this model is inherently inflexible. It presents a binary, take-it-or-leave-it proposition that doesn’t account for the varying and fluctuating liquidity needs of either the buyer or the seller. A buyer might have the cash available on day 12 but has no incentive to pay before day 30, while a seller might desperately need the cash on day 5 but has no mechanism to offer a slightly larger discount to receive it.

Dynamic discounting fundamentally breaks this rigid structure. It is a financial mechanism that offers early payment discounts on a sliding scale, where the size of the discount is directly proportional to how early the payment is made. Using a digital platform, a supplier can see a range of options: for example, a 3.2% discount for payment on day 10, a 2.7% discount for payment on day 20, and so on. This empowers the supplier to choose the precise payment date that best suits their cash flow needs, transforming a rigid term into a flexible liquidity tool.

The AI-Powered Optimization Engine

While the concept of dynamic discounting is powerful on its own, AI elevates it from a useful tool to a highly intelligent strategic function. An AI-powered optimization engine makes the process truly dynamic and financially optimized. Instead of applying a single, pre-calculated sliding scale to all customers, the AI system can tailor the incentive offers in real time based on a multitude of factors.

The AI can analyze the company’s current and projected cash position, its cost of capital, and the opportunity cost of deploying that cash elsewhere. Simultaneously, it can assess the customer’s individual profile, including their payment history, credit risk, and past responsiveness to incentives. By synthesizing these variables, the AI can calculate and present the optimal discount offer for that specific customer at that specific moment—an offer that is attractive enough to incentivize early payment but is also financially advantageous for the seller. This moves the strategy from a blanket policy to a highly targeted, micro-segmented approach that maximizes the return on every dollar of discount offered.

The Economic Logic: Sharing the Savings of Efficiency

A core strategic advantage of an AI-driven approach is its ability to perform a real-time cost-benefit analysis. The cost of chasing a client for payment—including staff time, communication expenses, and the opportunity cost of delayed cash—is a significant operational expense. An AI model can quantify this “cost to collect” for different customer segments and compare it against the cost of offering an early payment discount. The system can then find the optimal balance point, offering a discount that is less than the projected collection cost but still valuable to the customer. In effect, the AI intelligently divides the savings gained from avoiding a lengthy collections process between the seller and the buyer, creating a financially sound, win-win scenario that incentivizes the desired payment behavior.

Quantifying the Impact on DSO and Working Capital

The primary and most direct impact of a dynamic discounting program is a significant reduction in Days Sales Outstanding (DSO). By providing a compelling financial reason for customers to pay early, businesses can dramatically accelerate their cash conversion cycle. This acceleration directly unlocks cash that was previously trapped in accounts receivable, leading to substantial improvements in working capital and liquidity.

The financial benefits are tangible. Well-executed programs can lead to a 20% to 40% improvement in free cash flow as the gap between invoicing and cash receipt narrows. The value of these discounts can be surprisingly high when annualized. For example, capturing a seemingly small 2% discount by paying 20 days early on a “net 30” invoice translates to an annualized return of approximately 37%. For many businesses, this return far exceeds what they could earn on idle cash or the interest paid on short-term credit facilities, making it a highly attractive use of funds.

Strategic Value: Forging Stronger Customer and Supply Chain Relationships

The immediate financial benefits of improved cash flow for the seller and cost savings for the buyer are the primary and secondary effects of dynamic discounting. The third, and arguably most critical, strategic benefit lies in the strengthening of the entire commercial ecosystem. When a company provides its customers or suppliers with a flexible, valuable, and easily accessible source of liquidity, it transforms the relationship from purely transactional to truly collaborative.

This goodwill is not just an intangible benefit; it translates into concrete competitive advantages. Research indicates that suppliers who benefit from such programs are more likely to offer prioritization during times of resource scarcity and that the collaborative nature of the system in extreme cases can lead to a 55% reduction in supplier disputes and delays (from 45 days of average delays to 20). In an era defined by economic uncertainty and increasingly fragile global supply chains, building this kind of resilience and partnership is invaluable. Dynamic discounting, therefore, becomes more than just a cash management tactic. It is a powerful strategic tool for building more robust, loyal, and resilient supply chain relationships, providing a long-term competitive advantage that can be far more valuable than the immediate financial gain of the discount itself. Moreover, these incentives can also be used for future order discounting, potentially causing additional purchasing behavior or increased loyalty.

Chapter 6: Advanced Risk Analysis and Bad Debt Prevention

The ability to accurately assess credit risk is a foundational element of a healthy order-to-cash cycle. Extending credit is essential for facilitating B2B commerce, but it inherently carries the risk of late payments and, ultimately, bad debt. The goal of a modern, AI-driven O2C cycle is to proactively prevent bad orders from entering the system while simultaneously accelerating orders from good payers. The application of advanced machine learning (ML) provides a predictive shield, enabling businesses to move from reactive debt collection to proactive risk prevention, thereby protecting the bottom line while enabling safer growth.

The Power of Machine Learning on Complex Data

Conventional credit risk models are limited because they rely on clean, structured, and often historical data points like credit bureau scores and financial statements. The real world, however, is messy. The true indicators of financial distress are often hidden within vast, incoherent, and even completely unstructured datasets—like the text of emails, communication logs, and disparate market signals.

This is where machine learning becomes indispensable. ML algorithms have the unique ability to sift through this complexity, processing thousands of data points to find subtle, non-linear patterns that are invisible to human analysis and traditional models. It is this capability—to make sense of messy, multi-faceted data at scale—that makes modern risk analysis feasible. The performance uplift from this approach is dramatic. One highly tailored case study showed an ML model successfully identifying 83% of the bad debt that the traditional credit scoring system had completely missed. Just as importantly, the model’s precision allowed the bank to safely extend loan offers to 77% more people while maintaining its existing default rate.

Beyond Data: The Personalized Relationship Score

But even the most advanced external analysis misses a fundamental truth of business: who gets paid first? When cash is tight, companies don’t pay the creditor with the highest risk score; they pay their strategic partners. A company’s public financial health is one thing, but the strength of the specific relationship you have built with them is an entirely different—and often more powerful—predictor of payment.

This is why the MaxCredible toolkit introduces a Personalized Relationship Score. This proprietary metric moves beyond simply checking external data sources and integrates deep, personal data from your entire history with a customer. It analyzes:

- The history of your interactions and the quality of your touchpoints.

- The speed and sentiment of their email replies.

- Their history of collaborative dispute resolution.

- The overall health and trajectory of the relationship itself.

By mixing external financial data (the “what”) with this deep internal relationship data (the “why”), the system builds a far more accurate and holistic picture of risk. More importantly, the MaxCredible toolkit is designed to actively improve this score, using the pillars of intelligent communication (Chapter 1) and smart incentives (Chapter 5) to elevate your status from a simple supplier to an indispensable strategic partner.

From Static Checks to Dynamic, Relationship-Aware Management

This holistic score enables a transition from a one-time, static credit check to a highly accurate continuous, dynamic risk monitoring process. The AI system monitors a customer’s account in real time, analyzing not just payment patterns but the health of the relationship itself. Some use cases with a very healthy supply of data have seen AUC scores of up to 0.994 (almost perfect classification of risk). The underlying truth of all these models is that the data is always leading, meaning the higher the volume and quality of data the better the model can be. As MaxCredible ties in very big data sets with a few hundred dimensions per invoice and debtor the models are set up to achieve up to 95% predictive accuracy (depending on the availability of this data per user). This effectively allows for dynamic credit limits, where the system continuously learns from this blended data to adjust credit lines up or down, ensuring that credit exposure is always aligned with the true, holistic reality of the customer relationship.

Strategic Value: Agentic AI, Explainability (XAI), and Governance

This data-rich, relationship-aware approach to risk culminates in the development of truly autonomous systems. A compelling example is Eloquent AI, a company that has gained significant attention for its compliance-first approach. Their system is designed to mimic and learn from the decisions made by human experts. By modeling expert human behavior, the AI’s actions—whether in credit checking or policy validation—remain aligned with established business logic and are therefore inherently explainable. This methodology allows them to automate up to 96% of the end-to-end process, creating a truly agentic AI that can take over the full workload.

This concept of agentic AI is also emerging in other parts of the O2C cycle, such as autonomously negotiating payment plans within predefined business rules. However, the power of these systems introduces a critical challenge: the “black box” problem. In the highly regulated world of finance, a business cannot defend a credit decision if it cannot explain the logic behind it.

This makes Explainable AI (XAI) an essential component. Tools like LIME and SHAP provide human-understandable explanations for a model’s decisions, even when those decisions are based on complex, multi-faceted data like a relationship score. With regulations like the European Union’s AI Act classifying credit scoring systems as “high-risk,” the path forward is clear. The true strategic imperative is to build a comprehensive and defensible risk management system—one that combines predictive models with robust XAI capabilities and a rigorous governance framework. In MaxCredible’s philosophy and product there’s a deep focus on the score narrative, showing understandable and interpretable subscores but also descriptive behavior such as “responsiveness to payment/reminder strategies”. In the world of credit risk, accuracy is ultimately worthless without explainability and compliance.

Chapter 7: The Self-Learning System: Autonomous Dunning Strategy and Experimentation

In the pursuit of optimizing credit management, the final and most advanced frontier is the creation of a system that not only executes strategies but also autonomously learns, adapts, and improves them over time. While other pillars focus on what to communicate (GenAI) or who to prioritize (risk models), this pillar addresses the meta-level question of how to continuously discover the absolute best strategy for every customer in every situation. This involves moving beyond traditional, static testing methods to embrace dynamic, real-time experimentation engines that create a perpetual feedback loop of improvement.

From A/B Testing to Complex Multivariate Experimentation

The traditional method for comparing the effectiveness of different strategies is A/B testing, also known as split testing. In the context of collections, a team might test two different email subject lines (Version A vs. Version B) by sending each to 50% of a customer segment and measuring which one results in a higher payment rate . This method is valuable but has inherent limitations. It is a slow process that must run for a statistically significant period, during which 50% of the audience is intentionally shown the inferior version . Most importantly, it typically tests only one variable at a time, making it a cumbersome way to optimize a complex, multi-faceted communication strategy.

A more advanced approach is multivariate testing (MVT), which allows for the simultaneous testing of multiple variables and their interactions. For example, a team could test two different headlines, three different message tones, and two different call-to-action buttons all at once. The system would create and test all possible combinations (2 x 3 x 2 = 12 variations) to identify not just the best individual elements, but the most powerful combination of them. This provides a much deeper level of analysis but requires a very large volume of traffic to be effective.

The Multi-Armed Bandit (MAB): Real-Time, Autonomous Optimization

A far more advanced and efficient approach to experimentation is the Multi-Armed Bandit (MAB) algorithm. The name comes from a classic thought experiment involving a gambler facing a row of slot machines (or “one-armed bandits”). The gambler’s goal is to maximize their winnings as quickly as possible. They must balance “exploration” (trying different machines to see which ones pay out) with “exploitation” (repeatedly pulling the lever of the machine they believe is the best) .

In a collections context, each “arm” of the bandit is a different dunning strategy, which can be a complex combination of phrasing, media type, and timing . For example:

- Arm 1: A formal email sent 3 days after the due date.

- Arm 2: A friendly SMS reminder sent 5 days after the due date.

- Arm 3: A GenAI-crafted personalized message offering a payment plan on day 7.

- Arm 4: A phone call from an automated voice assistant on day 10.

Unlike a traditional test that would rigidly assign 25% of customers to each arm, a MAB algorithm starts by exploring all options but quickly and dynamically begins to favor the ones that are performing better in real time . If, after a short period, the algorithm observes that Arm 2 (the SMS reminder) is generating the highest rate of immediate payments, it will automatically start sending a larger percentage of customers down that path—perhaps 40% to Arm 2, and 20% to each of the others. It continues to explore the other options with a smaller portion of the traffic, but it dynamically allocates the majority to the current winner. This approach minimizes “regret”—the value lost by showing customers a suboptimal strategy—and maximizes results during the experimentation phase, not just after it .

Contextual Bandits: The Pinnacle of Personalization

The concept can be elevated even further with the use of “Contextual Bandits.” A standard MAB algorithm seeks to find the single best strategy for the entire user base. A Contextual Bandit, however, learns to find the best strategy for a given context or customer segment.

The algorithm is fed contextual information about each customer—such as their risk score, payment history, industry, or company size. It then learns complex relationships, such as discovering that Strategy A (a gentle email) is the most effective for low-risk, long-term customers, while Strategy B (an assertive SMS) works best for high-risk, new customers. The system then applies these optimized strategies automatically and individually, without any human intervention or pre-defined segmentation rules. It essentially creates a hyper-personalized optimization engine that matches the perfect outreach strategy to the perfect customer profile in real time.

Strategic Value: Creating a Continuously Improving Collections Engine

The first-order view of this pillar is that MABs are simply a more efficient way to conduct A/B tests. The second-order view is that they automate the process of strategy optimization. The ultimate strategic value, however, is that this pillar functions as the “meta-layer” or the intelligent engine that powers and continuously improves all other communication-based pillars within the credit management framework.

This creates a powerful, perpetual feedback loop. A generative AI system (Pillar 1) can create a virtually endless number of variations of a dunning email—different tones, different calls to action, different subject lines. A smart incentive system (Chapter 5) can offer a wide spectrum of discount options. A MAB algorithm can then take all of these potential strategies and autonomously and continuously test them against each other in the real world, in real time. It will automatically discover and deploy the optimal combination of message, timing, channel, and incentive for every micro-segment of the customer base.

This pillar, therefore, represents the most advanced and “geeky” form of automation in the credit management stack. It is the mechanism that ensures the entire system is not static but is constantly learning, adapting, and evolving towards peak performance. It is the final piece of the puzzle that enables the creation of a truly self-learning and self-optimizing collections and credit management function.

Conclusion: Synthesizing the Impact and Acknowledging the Gaps

The seven pillars of AI-driven credit management represent a comprehensive and transformative framework for modernizing the order-to-cash cycle. When viewed not as isolated technologies but as an integrated system, their cumulative effect is profound, creating a finance function that is proactive, intelligent, efficient, and customer-centric. However, a truly strategic implementation requires looking beyond these operational pillars to address the foundational elements of governance, regulation, and the broader financial ecosystem.

The Cumulative Effect: A 360-Degree View of Transformation

The synergy between the seven pillars creates a virtuous cycle of continuous improvement. The journey begins with a foundation of advanced risk analysis (Chapter 6), where machine learning models move beyond static scores to provide a dynamic, predictive understanding of customer behavior. This deep insight informs the actions of the entire system. It allows for proactive, hyper-personalized outreach crafted by Generative AI (Chapter 1), ensuring that every communication is empathetic, relevant, and effective.

The performance of these communications is not left to chance; it is relentlessly optimized in real time by autonomous experimentation engines like Multi-Armed Bandits (Chapter 7), which continuously discover the best strategy for every customer segment. This intelligent engagement encourages faster payments, which are further incentivized by AI-powered dynamic discounting (Chapter 5) and processed seamlessly through smart, automated payment systems that minimize failures and churn (Chapter 3). The entire operational workflow, from order entry to cash application, is streamlined by end-to-end automation, eliminating manual friction and cost (Chapter 4). Guiding this entire intelligent operation is a highly accurate, AI-driven cash flow forecast (Chapter 2), which provides the strategic visibility needed for confident financial planning.

Together, these pillars deliver a holistic transformation, driving down DSO, unlocking working capital, slashing operational costs, mitigating bad debt, and, most importantly, turning a potentially negative collections process into a positive driver of customer retention and loyalty.

The Omitted Pillars: Essential Foundations for Success

While the seven pillars provide a powerful operational roadmap, a durable and successful AI transformation in credit management rests on several foundational elements that were not explicitly detailed in the initial scope but will increase in importance in the upcoming years. These “omitted pillars” are not optional add-ons but essential prerequisites for long-term success and responsible implementation. Future whitepapers will include them as staples and mandatory assets for each of the pillars.

Omitted Pillar 1: AI Governance and Model Risk Management: The power of AI models comes with inherent risks. Models can “drift” over time as underlying data patterns change, leading to a degradation in performance. They can also perpetuate hidden biases present in historical data. A robust AI governance framework is therefore critical. This includes processes for ongoing model monitoring, periodic validation, and clear protocols for managing incidents when a model behaves unexpectedly. Without such governance, even the most accurate model can become a liability, making unsound decisions and exposing the organization to financial and reputational risk.

Omitted Pillar 2: The Regulatory and Compliance Landscape: The use of AI in finance, particularly for credit decisions, is coming under intense regulatory scrutiny. Frameworks like the EU’s AI Act and data privacy laws like GDPR impose strict obligations on businesses . Credit assessment systems are often classified as “high-risk AI,” mandating transparency, explainability, and human oversight. Compliance can no longer be an afterthought; it must be a core design principle embedded in the development and deployment of any AI system used in credit management. Navigating this complex legal landscape is essential for avoiding significant penalties and maintaining the license to operate.

Omitted Pillar 3: A Holistic View of Supply Chain Finance (SCF): Focusing solely on the seller’s accounts receivable (the O2C cycle) provides only half of the picture. A company’s cash flow is equally dependent on its management of accounts payable. AI is also revolutionizing this side of the equation, as well as the sophisticated financing mechanisms that strategically connect buyers and suppliers, such as self-serving, collaborative cashflows (allowing two-way credit lines tied to cashflow), and reverse factoring. A truly strategic approach to working capital optimization requires a holistic view of the entire supply chain finance ecosystem, using AI to balance inflows and outflows intelligently and collaboratively with trading partners.

Final Outlook: The Future of the Autonomous Finance Function

The convergence of these seven operational pillars with the foundational requirements of governance, compliance, and a holistic supply chain perspective points toward a clear future: the emergence of the autonomous finance function. This will be a department defined not by manual transactions and reactive problem-solving, but by data-driven strategy and continuous, automated optimization. The role of the human finance professional will be elevated from processor to strategist, overseeing an intelligent system, interpreting its insights, and making the high-level decisions that drive growth. The ultimate vision is a credit and cash flow management function that is not only supremely efficient but also contributes to building stronger financial health and more resilient relationships for both the company and its entire network of customers and partners.

Glossary

| Term | Definition |

| A/B Testing (Split Testing) | A method of comparing two versions of a single variable (e.g., two different email subject lines) by showing them to a split audience to determine which one performs better. |

| Agentic AI | An advanced AI system that can operate autonomously to achieve a goal. It can plan, make decisions, and use various tools without direct human instruction, such as managing a collections case from start to finish. |

| Artificial Intelligence (AI) | A broad field of computer science focused on creating systems that can perform tasks that typically require human intelligence, such as decision-making, understanding language, and recognizing patterns. |

| Contextual Bandits | The most advanced version of a Multi-Armed Bandit algorithm. It learns to find the best strategy not for a general audience, but for specific customer segments based on their unique “context” (e.g., risk score, payment history). |

| Days Sales Outstanding (DSO) | A financial metric measuring the average number of days it takes for a company to collect payment after a sale. A lower DSO indicates better cash flow and a more efficient collections process. |

| Dynamic Discounting | A flexible early-payment incentive where the discount offered to a customer is on a sliding scale, directly proportional to how early the invoice is paid. |

| End-to-End Automation | The process of creating a fully automated workflow for an entire business function (like Order-to-Cash) with minimal to zero human intervention. |

| Explainable AI (XAI) | A set of tools and techniques designed to make the decisions of complex “black box” AI models understandable to humans, providing clear reasons for a specific prediction or action. |

| Free Cash Flow (FCF) | The cash a company produces through its operations after subtracting for capital expenditures. It is a key measure of profitability and financial health. |

| Generative AI (GenAI) | A type of AI, powered by Large Language Models, that can create new, original content like text or images. It is used to draft hyper-personalized and empathetic customer communications at scale. |

| Involuntary Churn | The loss of a customer due to an unintended failure, most commonly a failed payment transaction (e.g., an expired credit card), rather than a conscious decision by the customer to cancel. |

| Large Language Models (LLMs) | The foundational technology behind Generative AI. LLMs are massive neural networks trained on vast amounts of text, enabling them to understand, summarize, translate, and generate human-like text. |

| Machine Learning (ML) | A subset of AI where systems are trained on large amounts of data to find patterns and make predictions without being explicitly programmed for that task. |

| Multi-Armed Bandit (MAB) | An autonomous approach to experimentation that dynamically allocates more traffic to the better-performing version of a test in real-time, maximizing results and accelerating learning. |

| Multivariate Testing (MVT) | A complex form of testing that compares multiple variables at once (e.g., different headlines, tones, and calls to action) to find the most effective combination. |

| Natural Language Processing (NLP) | A field of AI that gives computers the ability to read, understand, and interpret human language, used to analyze the sentiment and intent of customer emails and messages. |

| Optical Character Recognition (OCR) | A technology that converts documents like PDFs or scanned images into editable and searchable data, forming the first step in “touchless” invoice processing. |

| Order-to-Cash (O2C) Cycle | The entire business process covering all steps from receiving and processing a customer order to receiving and applying the payment. |

| Predictive Analytics | The practice of using data, statistical algorithms, and machine learning to identify the likelihood of future outcomes based on historical data. |

| Reinforcement Learning | A type of machine learning where an AI agent learns to make optimal decisions by performing actions and receiving rewards or penalties, allowing it to continuously improve itself. |

| Robotic Process Automation (RPA) | The use of software “bots” to automate repetitive, rules-based digital tasks. AI-driven automation is a more advanced form that adds intelligence and decision-making to these tasks. |

| Supply Chain Finance (SCF) | A set of technology-based solutions that lower financing costs and improve efficiency for buyers and sellers linked in a supply chain. Dynamic discounting is one form of SCF. |

| Working Capital | A measure of a company’s short-term financial health, calculated as current assets minus current liabilities. It represents the capital available to fund daily operations. |

Author(s): Stefan van Tulder, Marverick van de Beeten

Labels: Personalization and empathy in communication, Predictive cash-flow and forecasting, Payment solutions and smart processing, Automation in credit management, Working capital optimization, Credit risk analysis, Continuous improvement and experimentation.